Understanding the difference between business-to-business (B2B) and business-to-consumer (B2C)

payments can be complex. Acquiring trustworthy information might not always be straightforward, and

technical jargon can feel overwhelming. This is where Wegile steps in.

In this article, we will explore B2C payment types as well as B2b payment types, the difference

between B2B and B2C payments. Whether you seek an introduction to the fundamentals or a deeper

understanding, we’ve got you covered. Let’s get started!

What is B2B Transaction

Picture yourself managing a restaurant. You require various supplies such as food, utensils, and

plates, which you procure from a wholesaler. This wholesaler serves as your B2B partner. A

negotiation occurs, allowing you to acquire these supplies at a reduced cost compared to their

standard market price.

You fund the purchase using your resources and in sizeable quantity, in return, secure a discounted

price from the wholesaler. This instance exemplifies a B2B transaction: you, as the buyer, engage in

an exchange with another business, the seller, where goods and services are traded at a discounted

rate.

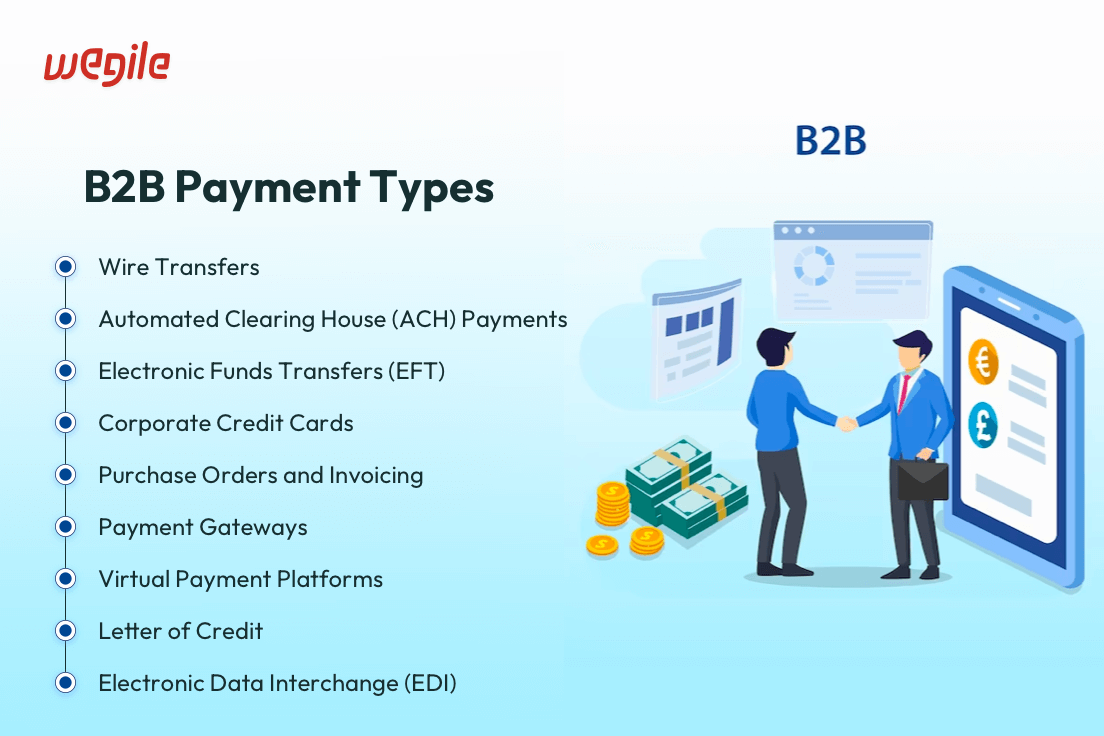

List of B2B Payment Types

-

1. Wire Transfers

Description: Wire transfers, also known as bank transfers, encompass the

electronic movement of funds directly between bank accounts.Advantages: This B2B payment type provides a secure and reliable avenue for

facilitating large-scale B2B transactions, both within the same country and across borders.Characteristics: The hallmark of wire transfers is their exceptional speed

and precision, making them particularly favored for transactions that necessitate immediacy

and assurance.Use Cases: Businesses widely employ wire transfers to settle invoices, make

payments to suppliers, and manage substantial financial transactions. -

2. Automated Clearing House (ACH) Payments

Description: ACH payments involve electronic transfers of funds within the

United States, conducted through the Automated Clearing House network.Advantages: Highly suitable for recurring B2B payments, such as monthly

bills and subscription services.Key Features: Notably cost-effective, ACH payments feature an automated

framework that enhances the efficiency of processing routine transactions.Usage: Commonly adopted by businesses seeking to automate regular payment

cycles. -

3. Electronic Funds Transfers (EFT)

Description: EFT encompasses the electronic transfer of funds between bank

accounts, often facilitated via secure networks.Advantages: EFT eliminates the need for paper checks, enhancing payment

efficiency and reducing processing time.Key Features: Widely used for recurring payments, including payroll

disbursement and supplier transactions.Usage: This B2B payment type is preferred for its reliability and speed in

managing frequent and routine fund transfers. -

4. Corporate Credit Cards

Description: Corporate credit cards are issued to businesses for making

payments related to goods and services.Advantages: Offers a combination of convenience, swift transactions, and a

transparent record of expenses.Key Features: This B2B payment enables businesses to capitalize on rewards

programs and cashback incentives.Usage: Frequently employed for various transactions, particularly those

requiring agility and ease of use. -

5. Purchase Orders and Invoicing

Description: Purchase orders (POs) are official documents used by businesses

to request goods or services from suppliers. Invoices are generated following the delivery

of goods or services, specifying the amount due.Advantages: This B2B payment type has a very structured approach with clear

terms and conditions, enhancing transparency in transactions.Key Features: Purchase orders initiate the transaction, while invoices

formalize payment obligations.Usage: Commonly utilized for organized and well-documented transactions in

B2B relationships. -

6. Payment Gateways

Description: Payment gateways are digital tools integrated into e-commerce

platforms and websites to facilitate secure online payment processing.Advantages: Ensures the security of financial information during B2B online

purchases.Key Features: Payment gateways are versatile, often accommodating multiple

payment methods such as credit cards, digital wallets, and bank transfers.Usage: Widely adopted in the digital landscape to enable safe and seamless

online transactions. -

7. Virtual Payment Platforms

Description: Virtual payment platforms, including PayPal, Stripe, and

Square, enable electronic fund transfers between businesses.Advantages: Offers a comprehensive array of payment methods, enhancing

flexibility and user convenience.Key Features: Provides businesses with a secure, easy-to-use digital

solution for managing payments.Usage: Prevalent in the digital era, especially for transactions requiring

multiple payment methods. -

8. Letter of Credit

Description A Letter of Credit (LC) is a financial instrument utilized

primarily in international B2B transactions, offering a guarantee of payment from a bank to

the seller.Advantages Provides assurance to both buyer and seller regarding payment

upon successful completion of the transaction.Key Features A bank issues the LC, acting as a mediator to ensure adherence

to the agreed terms.Usage Particularly crucial in cross-border transactions where trust and

payment assurance are paramount. -

9. Electronic Data Interchange (EDI)

Description EDI involves the electronic exchange of standardized documents

between businesses, streamlining transaction processes.Advantages Enhances efficiency by automating orders, invoices, and other

transaction-related information.Key Features EDI (B2B payment type) reduces manual data entry, thereby

minimizing errors and improving accuracy.Usage Commonly employed for large-scale transactions that require seamless

and efficient data exchange.

What is B2C Transaction

A B2C transaction, or Business-to-Consumer transaction, mirrors the scenario of a customer stepping

into a retail store and buying products or services. B2B payment involves an interaction between a

business and an individual consumer.

To comprehend this idea better, consider the analogy of placing an order for food delivery from a

restaurant. In this instance, the customer initiates a food order with the restaurant, anticipating

its delivery to their residence. Consequently, the restaurant furnishes a service (food delivery) in

exchange for the customer’s payment. In essence, this encapsulates the essence of a B2C transaction:

the business furnishes a service or item, and the customer compensates in return.

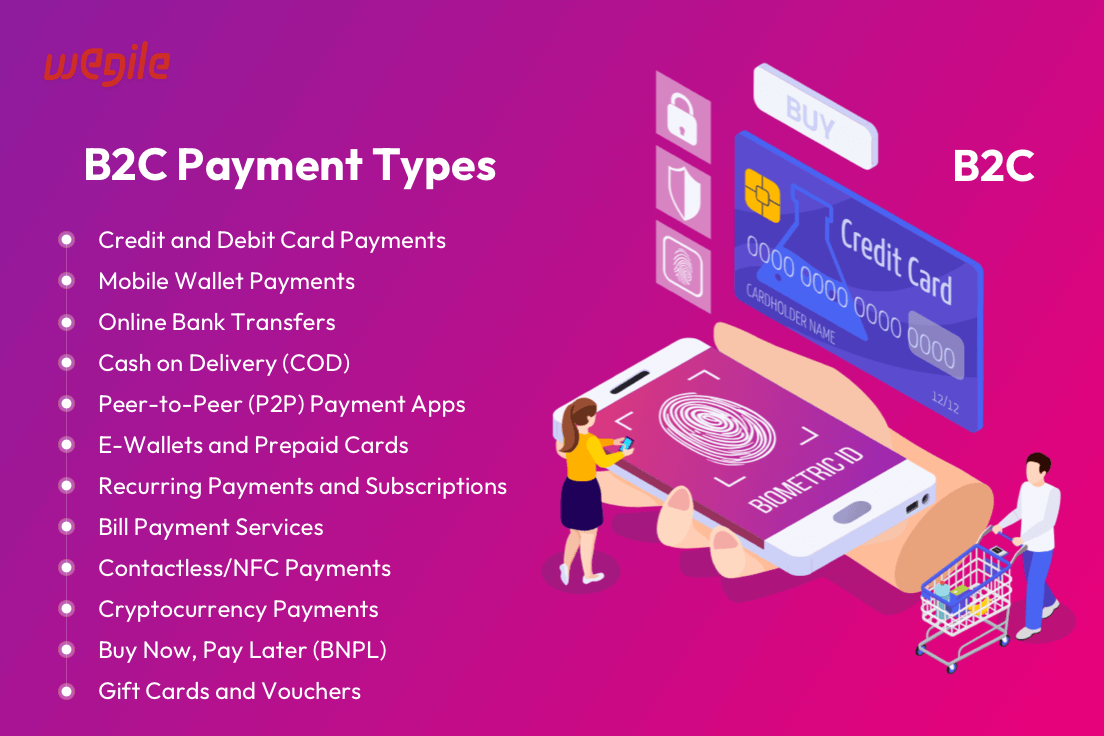

List of B2C Payment Types

-

1. Credit and Debit Card Payments

Description: Credit and debit card payments constitute a prevalent B2C

payment type, allowing customers to make purchases by electronically accessing their bank

accounts or utilizing credit lines.Advantages: Convenience, widespread acceptance, purchase protection, and the

ability to earn rewards (credit cards).Key Feature: Immediate payment or deferred payment with interest (credit

cards).Usage: This B2C payment type is widely used for online shopping, in-store

purchases, and bill payments. -

2. Mobile Wallet Payments

Description: Mobile wallet payments store payment information on

smartphones, allowing users to make contactless payments.Advantages: Speed, security, convenience, and the ability to store multiple

payment methods.Key Features: Near Field Communication (NFC) technology for contactless

transactions.Usage: Commonly used for in-store purchases, transportation, and mobile app

payments. -

3. Online Bank Transfers

Description: Customers pay directly from their bank accounts using online

banking platforms.Advantages: Direct and secure transactions, no need for a third party, and

often no fees.Key Features: Direct transfer from the customer’s bank account.

Usage: Online shopping, bill payments, and transferring funds to others.

-

4. Cash on Delivery (COD)

Description: Customers pay for their orders in cash upon delivery.

Advantages: Trust for those wary of online payments and the ability to

inspect goods before payment.Key Features: Payment occurs upon product receipt.

Usage: Common in regions with low online payment adoption or for high-value

purchases. -

5. Peer-to-Peer (P2P) Payment Apps

Description: P2P apps allow individuals to send money to others using a

mobile app.Advantages: Quick and convenient person-to-person payments.

Key Features: Simple and user-friendly

apps for transferring money.Usage: Splitting bills, repaying friends, and making informal payments.

-

6. E-Wallets and Prepaid Cards

Description: E-wallets store digital funds, and prepaid cards are loaded

with a specific amount of money.Advantages: Secure, convenient, and control over spending (prepaid cards).

Key Features: Digital storage of funds (e-wallets) or preloaded balance

(prepaid cards) are the key feature of this B2C payment.Usage: Online shopping, digital services, and budget control.

-

7. Recurring Payments and Subscriptions

Description: Customers subscribe to services and are billed automatically at

regular intervals.Advantages: Convenience, seamless service access, and cost predictability.

Key Features: Automated billing based on subscription terms.

Usage: Streaming services, software subscriptions, and membership clubs are

few example for this B2c payment type. -

8. Bill Payment Services

Description This B2c payment type uses online platforms for paying recurring

bills like utilities and rent.Advantages Centralized bill management, avoiding late payments, and setting

up recurring payments.Key Features Consolidated bill payment platform.

Usage Paying utility bills, rent, and other recurring expenses are the usage

for this B2C payment. -

9. Contactless/NFC Payments

Description This B2c payment type revolves around Contactless payments and

involve tapping a card or smartphone on a payment terminal.Advantages Speed, convenience, and enhanced security.

Key Features Use of NFC technology for contactless transactions.

Usage In-store purchases and public transportation.

-

10. Cryptocurrency Payments

Description Some businesses accept cryptocurrencies like Bitcoin for

payments.Advantages Security, transparency, and the potential for global

transactions.Key Features Use of blockchain technology for secure and decentralized

transactions.Usage Niche markets and tech-savvy customers.

-

11. Buy Now, Pay Later (BNPL)

Description BNPL lets shoppers make purchases and delay full payment by

spreading costs into manageable installments.Advantages BNPL offers financial flexibility, allowing consumers to afford

immediate purchases without upfront payment. It’s especially useful for larger expenses.Key Features Customers can choose to pay over time, often without interest

if paid within the agreed period.Usage Ideal for those needing products or services urgently but prefer

deferred payments. Common for electronics, fashion, and more. -

12. Gift Cards and Vouchers

Description Prepaid cards/vouchers let consumers buy specific items or

services with set value limits.Advantages This B2C payment makes for personalized gifts and provides

discounts or promotions. Businesses benefit from customer attraction and loyalty.Key Features Cards/vouchers have set values and can be digital or physical.

Usage This B2c payment type is popular as gifts during special occasions or

for accessing discounts and specific purchases from retailers and service providers.

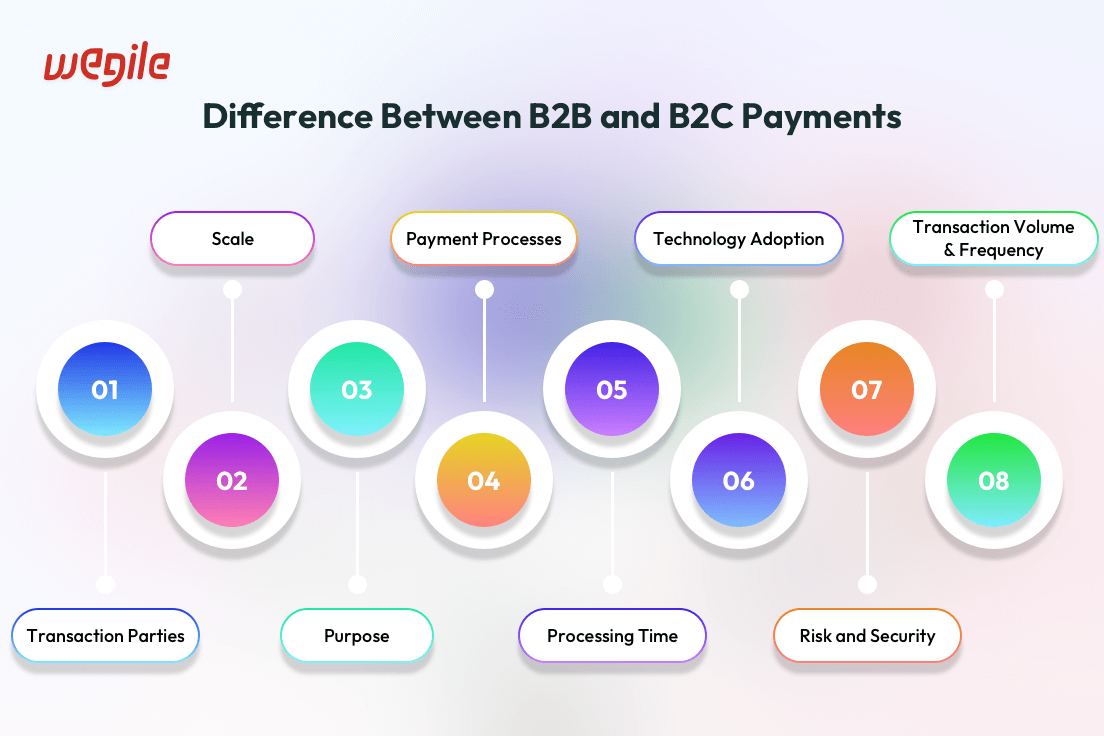

Difference Between B2B and B2C

Payments | B2B vs B2C Payments Comparison

| Sr.No | Aspects | B2B | B2C |

|---|---|---|---|

| 1. | Transaction Parties | Within business-to-business transactions, the participating entities on both ends of the exchange comprise corporate entities. |

Business-to-consumer (B2C) transactions are characterized by a solitary buyer, that being an individual consumer. |

| 2. | Scale | In B2B, the scale of operations is often much larger than in B2C. In order to service their clients, businesses typically need to have access to a broad range of resources, supplies, personnel, and technology – all on a much grander scale than what’s needed for consumer products and services. |

When it comes to B2C, the scale required is somewhat limited in comparison. Companies offering consumer goods and services only need enough resources to meet the demands of their customers. |

| 3. | Purpose | The fundamental objective underpinning B2B transactions is the facilitation of commercial interactions between two business entities. Such B2B transactions are supported by the necessity of enterprises to procure essential commodities, services, or raw materials from other businesses, thereby fortifying their internal operational frameworks. |

In contrast, B2C transactions are strategically orchestrated to furnish goods or services directly to consumers. This strategic approach aligns with the intention of addressing individual customers’ requirements, needs, and desires, thereby engendering a convenient and gratifying purchase journey. |

| 4. | Payment Processes | In B2B payments, the payment protocol conventionally encompasses the issuance of an invoice or a payment request dispatched by the business vendor to the business purchaser. This document outlines pertinent details and mentions the payment deadlines and amounts. The mode of disbursement could be a spectrum of options, spanning electronic payment platforms, conventional paper checks, or various forms of credit arrangements. |

B2C payments generally entail prepayment on the part of the consumer. The utilization of electronic payment methods such as debit and credit cards, digital wallets, and online banking services typify the norm for this category of transactions. In both scenarios, a paramount imperative remains—the adherence to all relevant legal and regulatory parameters to safeguard against fraudulent activities or other security threats. |

| 5. | Transaction Volume & Frequency | The primary difference between B2B and B2C payments or transactions hinges on the Transaction Volume & Frequency. In business-to-business, or B2B, transactions, one often encounters frequent, substantial-value transactions between two business entities. These b2b transactions can include the procurement of raw materials and components by manufacturers from their suppliers. |

B2C payment transactions usually include smaller purchases that happen more often due to impulse buying or returns. In contrast, B2B transactions might have bigger total amounts but lesser frequency, while B2C transactions tend to have lower overall amounts but happen more frequently. |

| 6. | Risk and Security | For any business engaging in B2B transactions, protecting confidential data and mitigating fraud should be a top priority. Fraudsters are always searching for potential vulnerabilities and with larger amounts of money at stake, it is essential that extra steps are taken to safeguard against these threats. Vigorous fraud prevention protocols are paramount since the risks are much greater and the financial implications much more significant. |

B2C payments frequently occur among unfamiliar parties, necessitating heightened measures to ensure transaction security. This involves employing supplementary authentication layers, leveraging encryption tools, and utilizing digital signatures. Moreover, due to limited control over consumer data usage, companies must implement safeguards like data anonymization and access management procedures to shield customers from potential fraudulent activities. |

| 7. | Technology Adoption | B2B transactions extensively use technology to optimize supply chain management, frequently employing advanced Enterprise Resource Planning (ERP) systems. Automation plays a crucial part in refining internal processes, boosting efficiency, and ensuring smooth communication between businesses. |

On the other hand, B2C transactions harness technology for seamless and convenient online payment processes, often incorporating tools like mobile wallets and e-commerce platforms. This tech-centric approach caters to the convenience of individual consumers in their digital transactions and interactions. |

| 8. | Processing Time | B2B transactions are usually larger in size and complexity than B2C transactions and, as a result, take longer to process. |

B2C transactions are relatively simple, involve readily available goods and can be quickly processed with few special considerations. As such, they generally take less time to complete than a B2B transaction. |

Leave a Reply